June 30 is an important day for American households. It is the time of the year when families receive statements from their stockbroker about the performance of their financial portfolios. Spoiler alert: Those statements don’t look pretty.

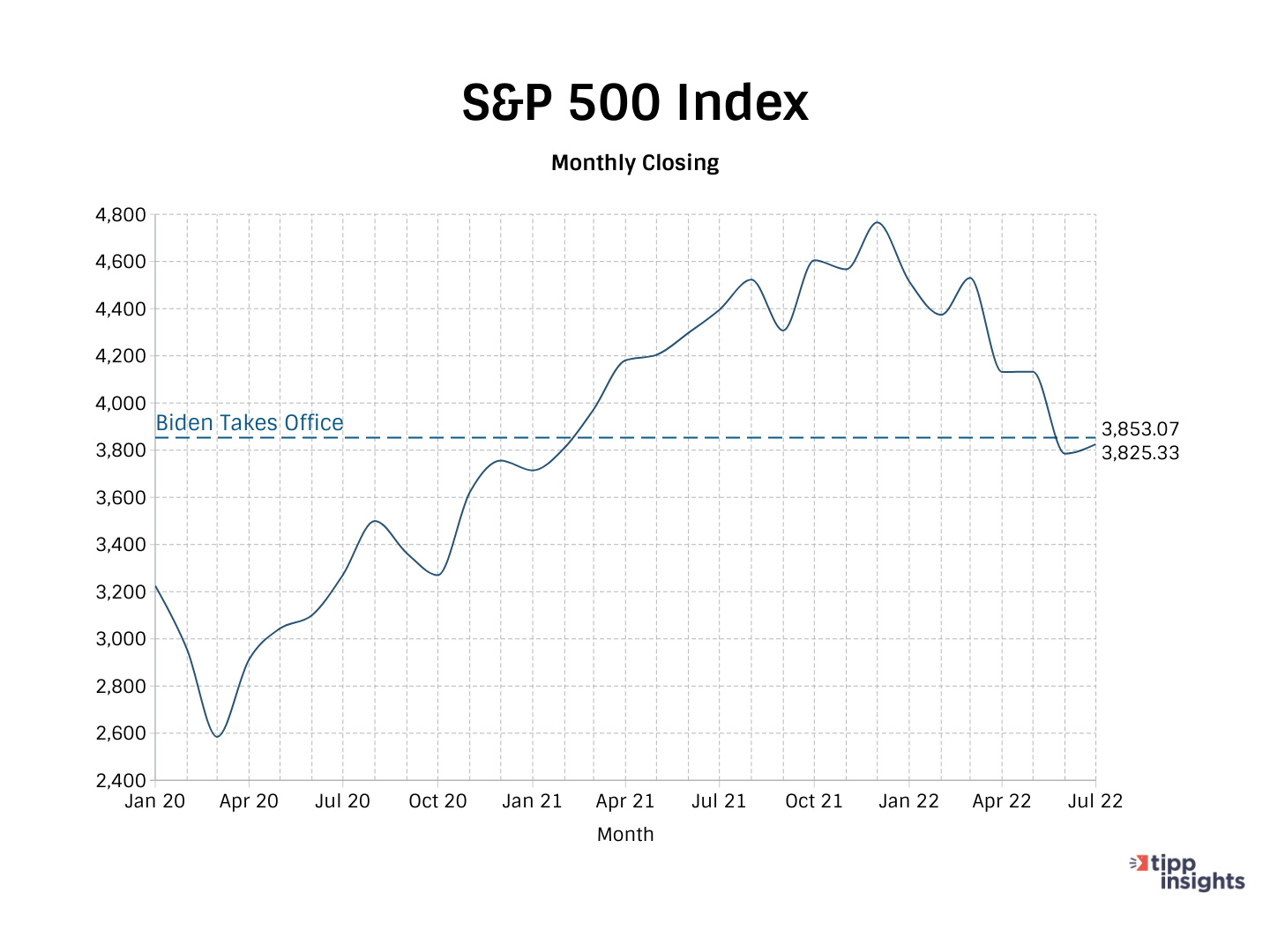

The S&P 500 index has fallen 21% since January. The tech-heavy Nasdaq is down 31%. The whopping declines have erased savings and retirement account gains since March 2020, when the pandemic and global shutdowns caused markets to crash worldwide. A feeling of helplessness has prevailed among millions of Americans even as the economy, on paper, began recovering after massive doses of federal spending.

For the average family, nothing has gone well since January 1 this year. Generous emergency federal support payments started during the pandemic stopped. The administration’s American Rescue Plan had increased the Child Tax Credit amount from $2,000 to $3,600 for qualifying children under age six and $3,000 for other qualifying children under age 18. President Biden sought a permanent increase in the child and dependent care tax credit in his Build Back Better plan – but it ultimately failed in the Senate because of the Left’s overreach in the House.

Inflation, which indicates a loss of purchasing power over time, was already eating into American family budgets. The media broadly covers rising gas prices and food costs at the grocery store. But the prices of every conceivable item or service – furniture, apparel, used cars, rental cars, airline tickets – have steadily increased, some by double-digit percentages, since May 2021.

The Fed, late in acknowledging the devastating effects of inflation, finally began to act in April. The Funds rate has increased by a remarkable 175 basis points in just three months, hurting millions of households. Families rely on borrowing for big-ticket items like homes, cars, higher education, and vacations. Mortgage rates, which have doubled since January 1, have caused the average American family with adjustable-rate mortgages to pay about $600 more each month to stay in their homes. Referring to Americans buying their first home, Glenn Kelman, chief executive of Redfin, a national real estate brokerage, said in the New York Times: “We’ve reached the point where people just can’t afford a house.” And we are only halfway into the interest rate hikes.

ADVERTISEMENT

The Fed also announced that it would stop buying corporate and treasury bonds, ending quantitative easing that showered the global economy with nearly $10 trillion in free cash pulled from thin air. Worse, the Fed also announced that it would begin to let bonds mature, meaning bond sellers must return scarce cash to the Fed at maturity. The massive mop-up exercise is intended to suck excess cash back into Fed vaults, depleting the economy’s money supply.

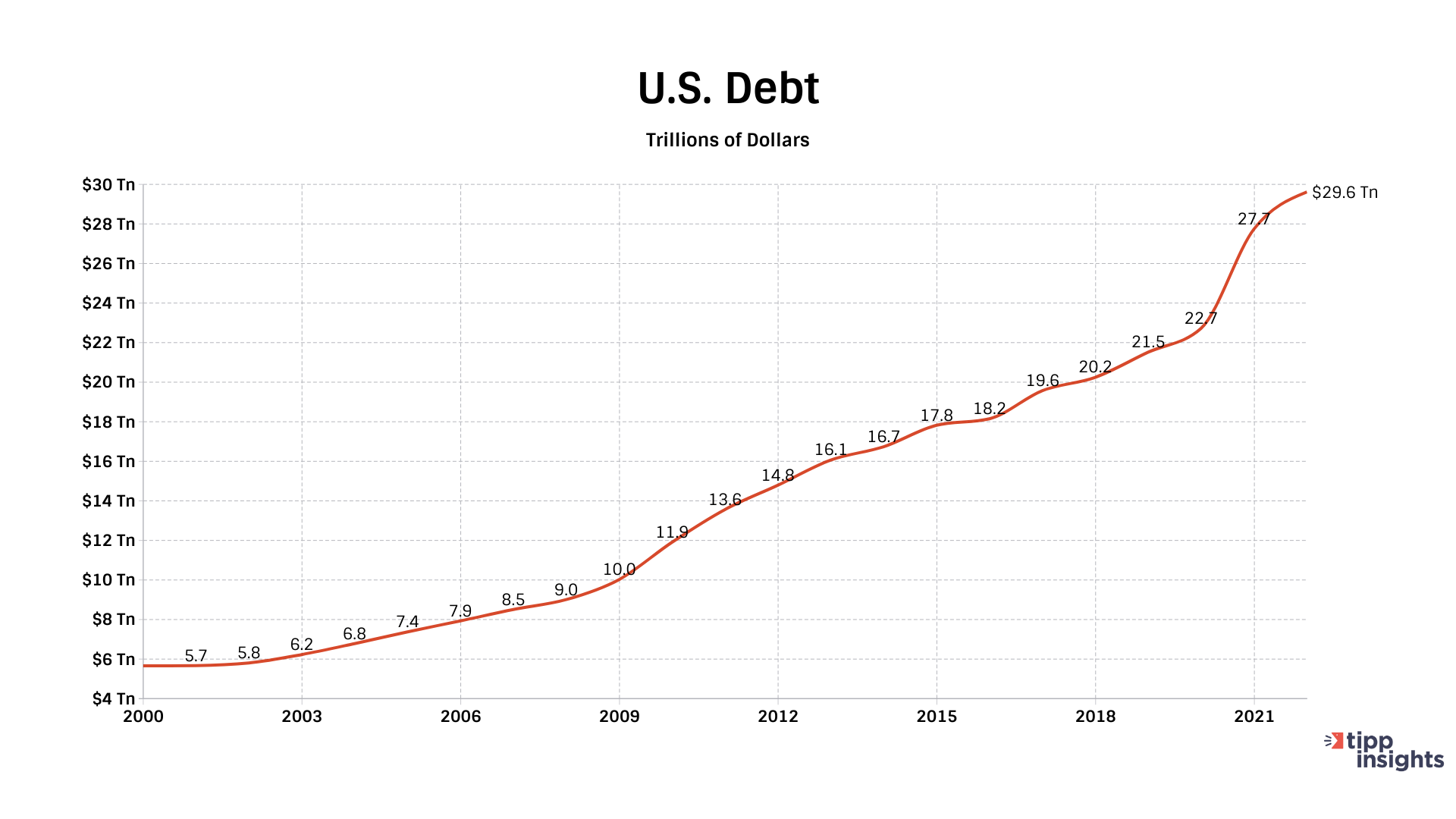

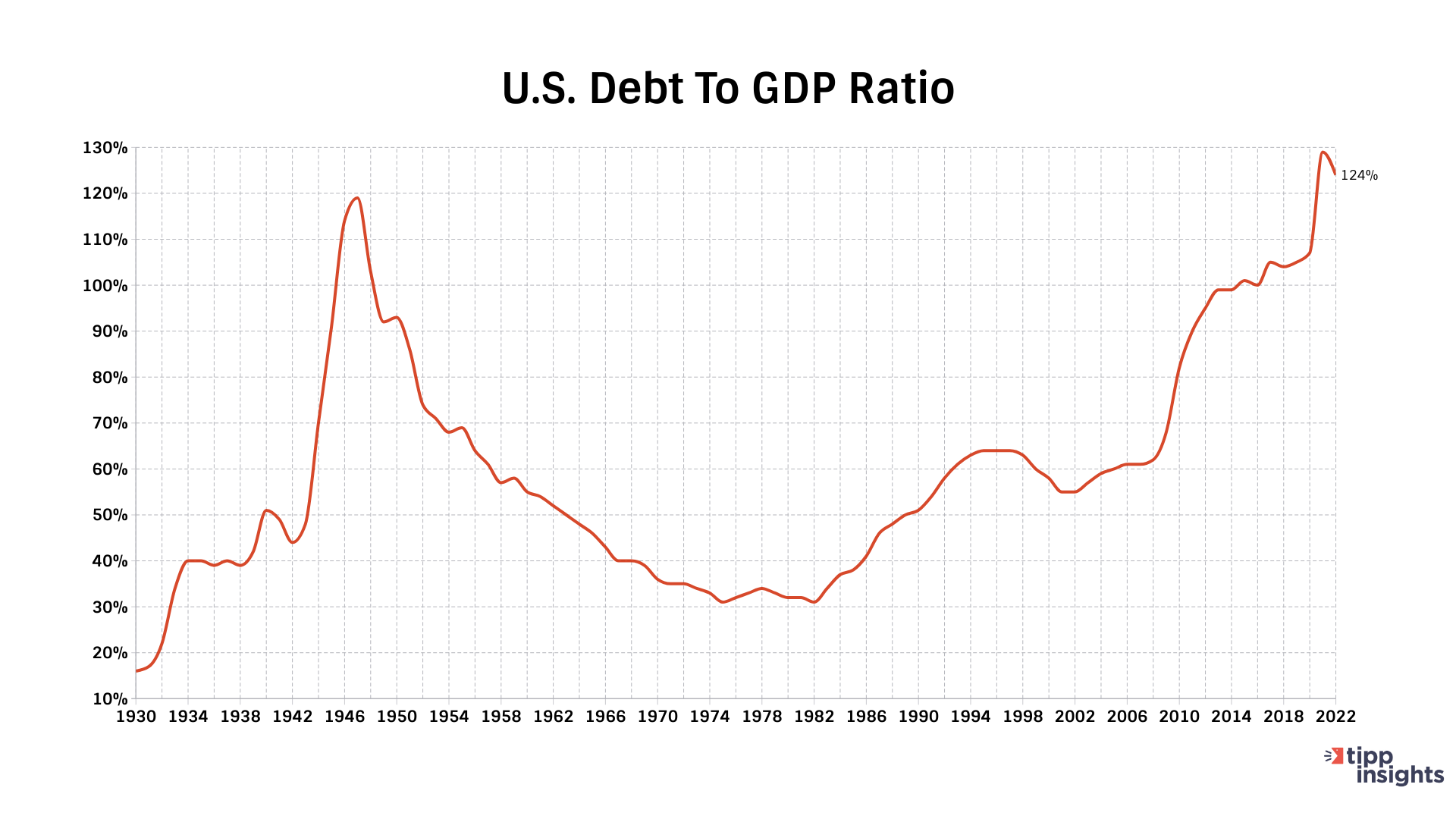

The country is now gripped with the polar opposite of “Irrational Exuberance,” a term that former Fed Chairman Alan Greenspan coined to describe America’s addiction to investing in dot-com companies in the mid-1990s. Those were glory days, by comparison. Under President Clinton and a Republican Congress, the federal government was operating under a balanced budget for the first time in over 50 years. The total federal debt was just $5.8 trillion, about 55% of GDP. Inflation was low, and the country was at full employment.

Today, everything is so different and far worse. The federal debt is $29.6 trillion, about 124% of GDP. Inflation is at 40-year highs and will likely keep going up for several months before turning around sometime in 2024. There is no appetite for increased government spending because excessive spending caused this mess. As interest rates rise, federal borrowing costs will increase to keep the lights on at federal agencies, further worsening the deficit.

It is little wonder that portfolio values are falling. Rising fixed investment yields tend to make investors pull money from securities and park it into bonds and certificates of deposit. Rising interest rates, which make lending expensive, discourage investors from borrowing and investing in securities.

Signs of a slowdown are everywhere. Tech companies, led by Tesla and Facebook, have announced layoffs or attrition plans in hiring. Some technology companies have begun withdrawing job offers made to new graduates. When tech slows, markets follow.

ADVERTISEMENT

Recent economic data suggests that the United States is likely in a recession, as defined by two consecutive quarters of negative growth. According to the Bureau of Economic Analysis’ third and final revision released on Wednesday, the U.S. GDP declined 1.6% annually in the first quarter of this year. The Atlanta Fed’s GDPNow gauge sees the second quarter at a negative 2.1%.

Furthermore, according to the June IBD/TIPP Poll, 53% of Americans believe the country is in a recession, surpassing 50 percent for the first time during Biden’s presidency.

The mind is a powerful enabler for both positive and negative thinking. With the summer season starting and American families limiting discretionary spending, nothing shocks them more than seeing that their hard-earned savings have been wiped out, leaving them in the deep-red territory. And like much else, they feel helpless, realizing that they are in a state of rational depression, only able to hope that things will turn around. They do know where to air their grievances. As Larry Kudlow says, the cavalry is coming in November.

We have no tolerance for comments containing violence, racism, profanity, vulgarity, doxing, or discourteous behavior. If a comment is spam, instead of replying to it please click the ∨ icon below and to the right of that comment. Thank you for partnering with us to maintain fruitful conversation.